All Categories

Featured

[/image][=video]

[/video]

You can't take a loan out on yourself, if there's no money to take a funding from. Make good sense? Now the fascinating thing is that when you're ready to take a funding out on yourself, the company you have the account with will offer you the quantity of cash you're trying to secure for a finance.

The cash will certainly never leave your account, and will proceed to produce and collect passion even WHILE your funding is still impressive. Example: So, state you have 500K in your account, and you take a finance from it of 500K. You will certainly have 500K in your hand to invest, spend, or do whatever with and at the same time you will still have 500K in your account growing on standard in between 57%, without risk.

Undoubtedly they can not provide you money for free for no factor. The outstanding part concerning this is that the cash being held as collateral remains in your account.

You want to pay it back on a monthly basis, due to the fact that it aids with development. This is a regular account so your regular monthly payment remains the exact same. You can enhance or lower the amount (yet it implies it will remain by doing this till the following time you transform it). We do not advise decreasing it unless press comes to shove and you have to, due to the fact that it negatively influences the development of the account.

People really try to boost it due to the fact that the manner in which compound passion functions: the longer you have the account open, and the even more you add, the better the growthThe firms that we use to open these accounts are FOR PROFIT business. That being said, a couple of things to keep in mind: While you are not using this money in this account, they are.

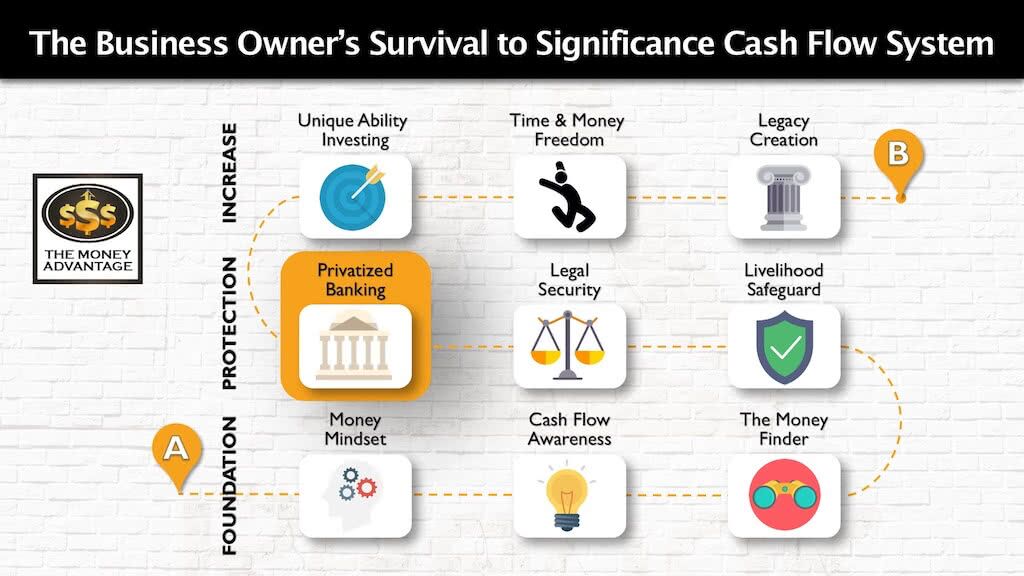

Whole Life Insurance Infinite Banking

This suggests makes it a win win for both partiesAnytime you hear the word 'funding' there is constantly an interest price connected with it. Generally speaking, usually the finance prices are around 45% however, despite having a lending outstanding, your cash is still growing in between 57% to make sure that suggests that you're still netting favorable development, despite a loan outstanding.

And last yet crucial caution, among the greatest barriers to getting going right now is that you require to have money conserved up first prior to you can take a finance out on your very own cash. There are lots of sensible benefits and strategies for using unlimited financial. You can utilize a boundless financial funding to repay points such as a vehicle, student lending, mortgage, and so on.

We are permanently really still expanding money, due to passion that we are still able to gather on our account. Below is an instance of this listed below: Example: Allow's check out a few different methods someone might buy a cars and truck for $50K. Choice 1 You pay $50K cash and you receive the automobile however your bank account has 50K much less.

This choice is worse than Alternative 1, because although you got the lorry, you lose 7,198.55 MORE than if you had paid cash money. This alternative is NOT chosen (however one that a lot of individuals take due to the fact that they do not recognize concerning various other alternatives.) Alternative 3 Suppose over those 5 years as opposed to settling the financial institution vehicle loan, you were putting $833.33 right into our represent boundless financial monthly.

Allan Roth Bank On Yourself

Currently of training course, the firm when you took the car loan out charged you a 4.5% rate of interest (typically bc the company needs to generate income in some way)So you lost $5,929 to the interest. But even after the financing interest is taken, the overall is $60,982 We still made an earnings of $10,982, as opposed to shedding $7198.55 to interest.

At our latest Sarasota Option Financial investment Club conference Rebekah Samples talked on the topic of "Just how to Become Your Own Bank and Leverage Your Cash." She talked briefly regarding the 5Fs: Belief, Household, Health And Fitness, Funds, and Flexibility. She said these are five points you need to do for yourself and you should not outsource them.

We need to assume concerning our money the very same means we believe concerning what we utilize money for. She talked regarding exactly how financial institutions offer out the money you down payment, they make a big revenue, which goes to their investors, and you obtain a little quantity of interest.

One way she talked around was via dividend paying entire life insurance plans, which permits you to use money deposited into them as your very own individual financial institution. Cash gained when the firm looking after the insurance coverage provides this money, goes back to you as a reward, and not to the investors.

We have been taught to think that saving up for something is better than obtaining money to buy it. She revealed a chart that displayed in both circumstances, we begin at no and get to zero, whether we borrowed and slowly settled the financial debt or we slowly conserved up then utilized the cash for the acquisition.

She stated dividend paying entire life insurance coverage prepares permit you to act as your very own financial institution with tax-free growth. This shows that there's a substantial void in comprehending the benefits these policies use beyond simply fatality advantages. The reality is, when done appropriately, utilizing life insurance coverage as your personal bank can work.but it doesn't always work (much more on that later).

Dive in to find out even more Welcome to the world of, a financial method that permits you to be your own financial institution. You can establish up your own financial system by taking out a whole life insurance plan and paying extra costs over and above the fundamental coverage amount.

{kind=link}

Latest Posts

Can You Be Your Own Bank

My Wallet Be Your Own Bank

Be Your Own Bank